Frank Manzo IV is the Policy Director of the Illinois Economic Policy Institute (ILEPI). Visit ILEPI at www.illinoisepi.org or follow ILEPI on Twitter @illinoisEPI. This post is part of the “Frankonomics” series.

All states collect tax revenues in some form. Typically, the primary method is through an income tax. Sales taxes and corporate taxes also play large roles in most states. In Kansas, the state was forced to increase sales taxes to make up a $400 million budget hole created after legislators slashed its income taxes and eliminated its top tax bracket. Finally, taxes on energy production taxes also play large roles in certain state budgets. State budgets that rely on the latter have recently fallen into chaos – especially Alaska (oil) and West Virginia (coal).

In the grand scheme of things, it does not matter that much how states decide to collect tax revenues. There are concerns about taxing “good” things– i.e., an income tax is an indirect tax on savings because workers have less take-home earnings to put in a bank or to invest. There are also concerns about the fairness of taxes– i.e., sales taxes are “regressive,” because poorer households spend a much larger fraction of their income on goods and services while wealthier families tend to have more savings. By cutting income taxes for the wealthiest but raising sales taxes, legislators in Kansas have made their system more favorable to the rich at the expense of lower-income households.

But, in general, there is no statistical relationship between lower state-level employment rates and higher personal income taxes, sales taxes, or corporate taxes per household.

Obviously, taxes have an impact at some high threshold. A personal income tax rate of 100%– at the very extreme– would discourage everyone from working. But taxes are relatively low in states across America. Even in California, where the top marginal income tax rate for millionaires is 13.3%, families in the Top 1 Percent only pay an effective tax rate of 8.6%.

In economics, a theoretical exploration of the threshold level where taxes start to become too burdensome is the “Laffer curve.” At the federal level, researchers have estimated that the optimal top income tax rate along the Laffer curve may actually be 68.4%, substantially higher than the current top marginal tax rate of 39.6%. Additionally, economists surveyed by the University of Chicago strongly disagree that a federal income tax cut “would raise taxable income enough so that the annual total tax revenue would be higher.”

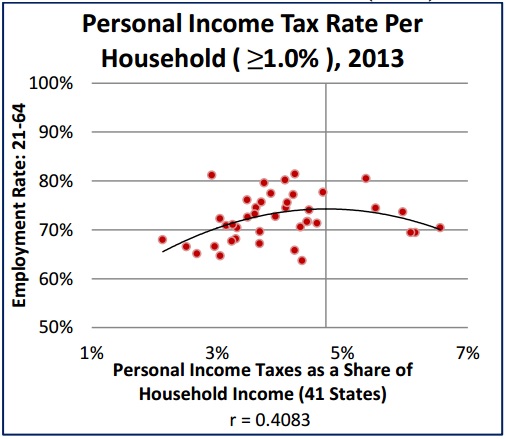

So what is the “Laffer curve” for state income tax rates?

Previous research by the Illinois Economic Policy Institute suggests the optimal personal income tax rate as a share of household income may be 4.74%. Using state-level data from 2013 for the 41 states that had an income tax, 4.74% is the threshold at which point the working-age employment rate tended to decline. Note that this is the effective tax rate for the average household.

This is particularly pertinent in the current budget discussion in Illinois. Except for fringe ideologues, basically everyone acknowledges that Illinois will need to cut spending AND raise revenues in order to Fix the Budget. On the revenue side of the equation, the Center for Tax & Budget Accountability (CTBA) has recommended– and the Illinois Economic Policy Institute (ILEPI) has separately proposed– raising Illinois’ flat personal income tax rate to 4.75%. The CTBA projects that a 4.75% personal income tax rate would raise about $3.3 billion while ILEPI estimates a $3.5 billion increase. Meanwhile, state-level data indicates that this increase is not likely to have very negative impacts on employment.

Illinois needs to get its state finances in order and its market economy back on sound footing. A 4.75 personal income tax rate– essentially the optimal point along the “Laffer curve,” using 2013 state level data– would help achieve both.